A potential economic recession and the supply chain bullwhip are colliding

Freight carriers across all modes should brace for weaker conditions in the coming months.

Subtext: Supply chains are experiencing a massive bullwhip from the COVID economy and have built up massive inventory levels. A slowdown in consumer spending caused by inflation and a potential recession will have a massive impact on freight demand and prolong an inventory drawdown.

As we look at the pandemic through the rearview mirror, the economy is shifting to a new phase. While the United States is currently experiencing full employment, American consumers are incredibly stressed about the state of the economy and personal financial security. Inflation, crashing stock markets, higher interest rates, and economic uncertainty are sapping any confidence that full employment should offer.

For supply chains, the consumer pullback couldn’t come at a worse time. The bullwhip effect has created a massive overstock of inventories and wreaked havoc on global supply chains as companies try to recover from the pandemic economy.

The bullwhip effect

The ‘bullwhip effect’ is a term used in supply chain circles to describe a scenario in which temporary surges in retail demand are magnified and exaggerated by upstream manufacturers and suppliers, who rapidly increase production well beyond the level that can be supported by consumers. Eventually, retailers find themselves with more inventory than they can sell, and what started as a goods shortage ends up as a goods surplus.

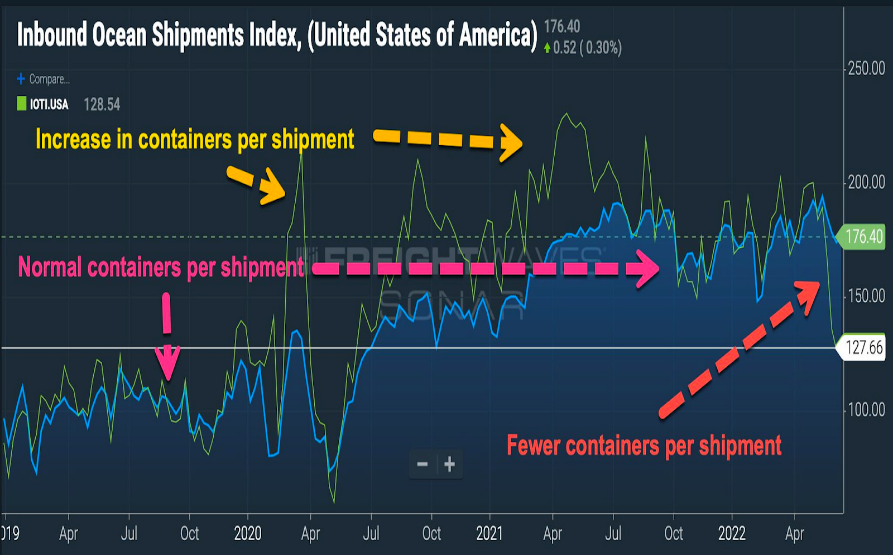

If there is a single chart that shows the supply chain bullwhip effect, it is this one:

Source: SONAR IOSI.USA (blue) IOTI.USA (green)

The chart displays an index of import shipments based on the number of bills of lading in blue and the corresponding container volumes in twenty-foot equivalent units (TEUs) in green. The two indices show how the ratio of containers to shipments has evolved during COVID.

Before COVID, the ratio of containers per shipment was fairly static and the two indices moved in tandem. Beginning in the summer of 2020, the container-to-shipment ratio exploded as Big Box retailers used their leverage to move more containers into their scheduled shipments. Smaller importers kept their container-to-shipment ratios more static, finding it harder to secure additional capacity on container vessels.

This continued until the fourth quarter of 2021, when Big Box retailers reverted to previous ratios, likely believing they had ample inventory on hand to handle demand.

At that point, had consumer demand levels remained stable, the bullwhip effect would have played itself out gradually, as retailers burned off higher levels of inventories over time.

But on February 24, 2022, the world completely changed. Russia invaded Ukraine. Energy and food prices surged in response, setting off inflation rates that the Western world had not seen since the early 1980s.

As inflation continued to accelerate into the spring, consumers pulled back spending on the very items they had previously consumed in excess. Retailers found themselves with even larger levels of inventories than previously forecasted and were forced to come clean in earnings reports and subsequent public announcements.

After results from the first quarter of 2022 and the subsequent announcements of excess inventories and slowing consumer sentiment, the Big Box retailers pulled back on the quantity of containers per shipment. After all, why would you continue to order more if you had more than enough in stock?

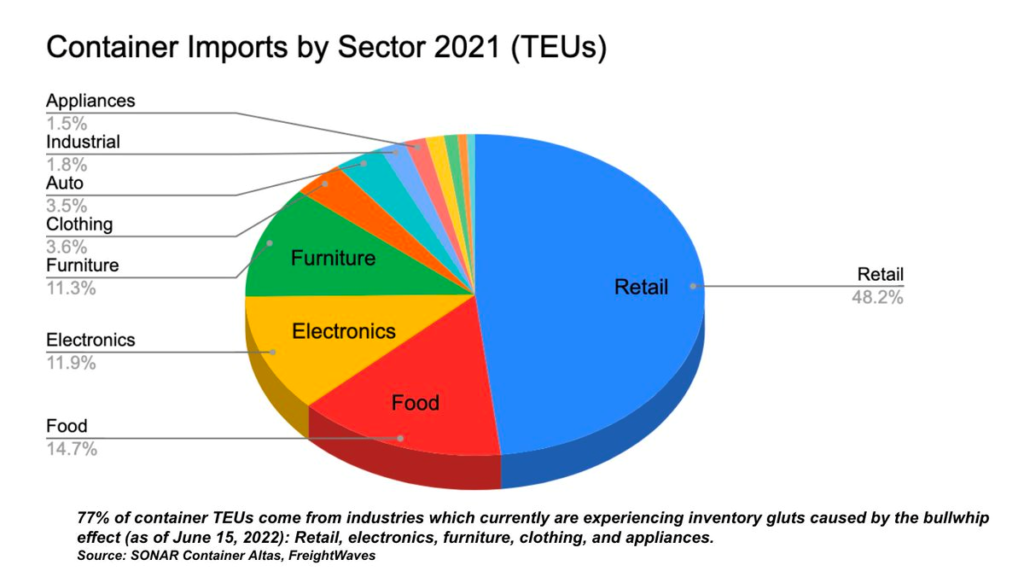

A full 77% of U.S. container imports come from industries that have reported massive supply gluts (retail, electronics, furniture, clothing, and appliances). FreightWaves anticipates continued weakness until inventories are worked back down to normal levels.

Walmart was the first major Big Box retailer to report having too much inventory. Target was the second. The two Big Box retailers also happen to be the two biggest importers of containerized freight into the United States. Between them, they imported nearly 1.7 million TEUs in 2021, representing nearly 7% of all U.S. container imports.

This past week, Nikkei Asia reported that Samsung was facing its own bullwhip effect of too much inventory and asked upstream suppliers to cut back production by as much as half in the month of July. Samsung was the seventh-largest importer into the United States in 2021. According to SONAR Container Atlas, Samsung imported 79,000 TEUs last month.

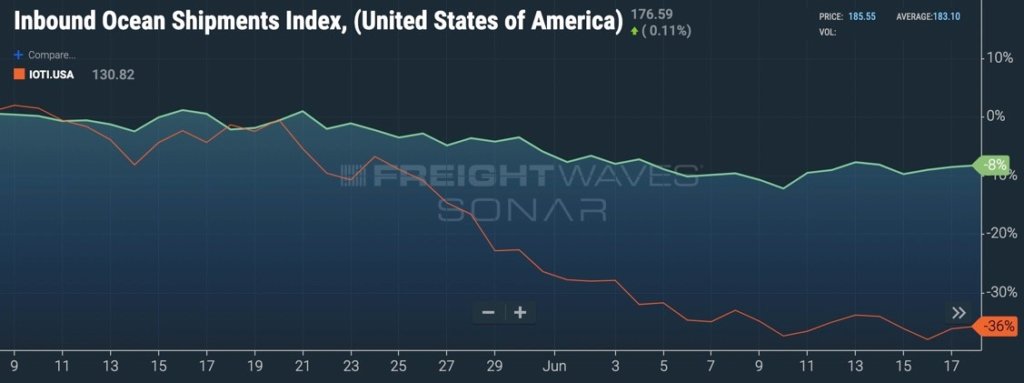

Source: SONAR Container Atlas

According to SONAR’s Container Atlas, on May 20th, the ratio of containers started to diverge again, this time dropping below pre-COVID norms. Since then, global shipment counts have dropped by 8% (green), while container bookings have dropped 36% (orange).

Source: SONAR IOSI.USA (green) IOTI.USA (blue)

Big Box retailers have responsive supply chains and can cancel orders quickly. Small importers tend to be slower to do so. They may not have the supply chain networks to respond to inventory issues as fast as the Big Boxes, but they also lack the leverage over their supplier networks to painlessly adjust orders up and down.

This softness in container markets will have a big impact on trucking in July, as the container slowdown hits North American ports.

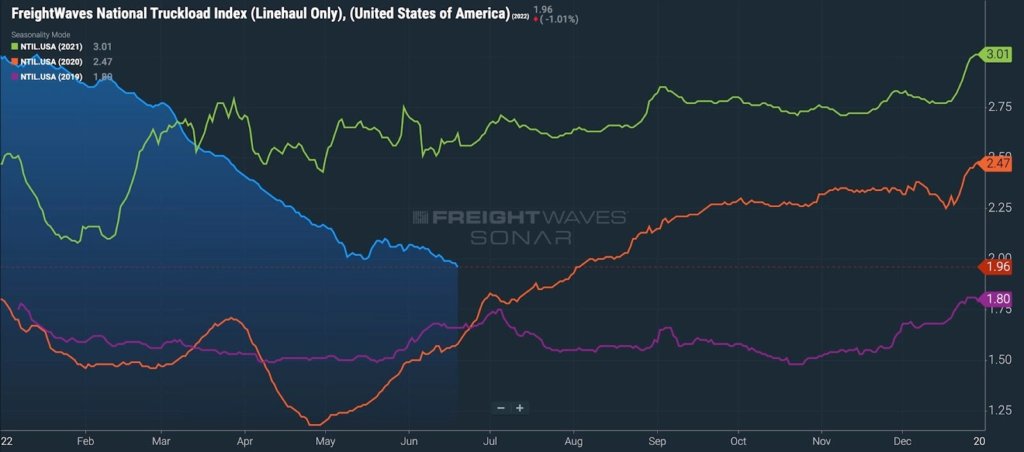

At this point in time, the trucking market continues to weaken. This is very concerning for mid-June (normally one of the hottest months in freight). The national spot index 7-day rolling average dropped from $2.07/mile on June 1 to $1.96/mile on June 20th.

Source: SONAR NTIL.USA

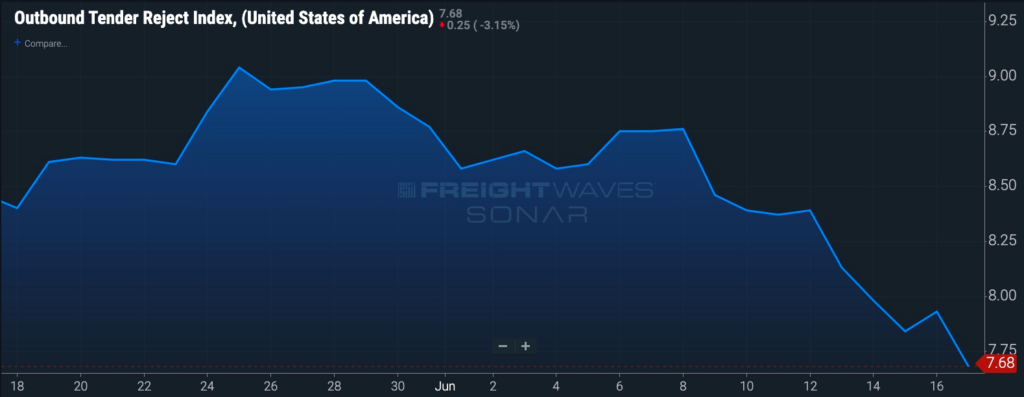

Tender rejections have dropped in the past week, hitting a new cycle low of 7.68%. Tender rejections are an indicator of trucking capacity conditions. Declining numbers indicate carriers are losing pricing power, while increasing numbers indicate carriers are gaining pricing power.

Source: SONAR OTRI.USA

Channel checks are now telling us that less-than-truckload (LTL) carriers (including the top-performing ones) are starting to see a slowdown. LTL is usually the last part of the market to feel a slowdown and the first to feel a recovery. LTL carriers handle smaller shipments from a wider portfolio of customers than truckload carriers, so they have more flexibility in maintaining shipment volumes and asset utilization through the cycle.

LTL is also more exposed to the industrial sector than truckload. We are also hearing that shippers (manufacturers, retailers, CPG, wholesalers) are seeing an acceleration in order cancellations and requests from customers to postpone deliveries.

There’s also a scramble for temporary warehouse space. Existing inventory isn’t selling at the expected prices, forcing companies to find incremental square footage to house newly arriving inventory. Shippers have slowed down moving containers out of the ports, causing container dwell times to lengthen.

Container spot rates continue to drop and should soon drop into negative year-over-year territory. The ocean carriers have far more pricing power than truckers do, but we don’t expect ocean container rate surges; in fact we expect the opposite – rates to continue to fall.

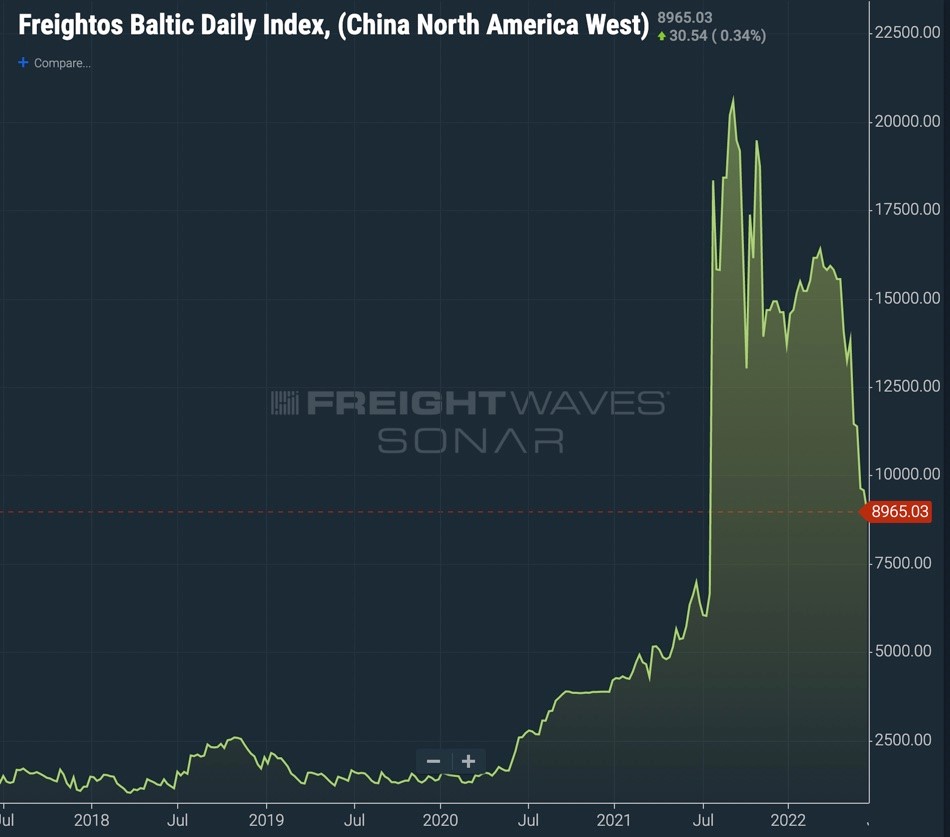

The weekly average of container spot rates from China to the U.S. West Coast has dropped from $15,551 on April 18 to $9,177 on June 16 – a drop of 41% – according to the Freightos Baltic Index.

The daily price updates, which are available to SONAR subscribers, shows that container rates fell from the last weekly update on June 16. The updated overnight spot rate on the China to North America West Coast trade lane on June 20 is $8,965.

Source: SONAR FBXD.CNAW

Fuel is still a major factor for anyone involved in freight movement. Diesel continues to surge higher and is within spitting distance of $6.00 on a national level ($5.85/gallon).

Source: SONAR DTS.USA

Diesel powers the industrial economy. Freight, farming, and construction all depend on diesel. As the price of diesel surges, it hurts the cash flow of companies across the economy and makes the Federal Reserve’s job harder in tamping down inflation.

July and August are always slower markets for freight – the so-called ‘summer doldrums.’ The conditions we currently see suggest that carriers should brace for even weaker conditions than normal. The Atlanta Fed’s high-frequency GDP tracker indicates the U.S. economy is already in a recession.

For the freight markets and supply chains, it couldn’t come at a worse time.

Interested in staying on top of what’s happening in the global physical economy? Check out SONAR, which provides the most comprehensive high-frequency supply chain data.

Get in touch with us!

4444 Wyoming Ave. Detroit, Michigan 48216 | Phone: 313-965-8299 | Fax: 313-965-7399

For more information on Cavalry Logistics International, please visit www.shipwithU.com/international.

For more information on Universal Logistics Holdings, Inc., visit www.universallogistics.com.